Bishop guides clients with their various estate planning needs and helps them navigate the Medicaid system in Florida. Bishop also represents clients worldwide in front of the IRS. Bishop is also a V.A. accredited attorney and helps Veterans obtain benefits from the Department of Veterans Affairs.

Kerven began his legal career as a criminal law attorney and was an assistant prosecutor for 7 years. Prior to joining Daily, Montfort, and Toups, Kerven served as the General Counsel for Florida’s Department of Military Affairs, where he was the chief legal and ethics officer for the state agency.

Share

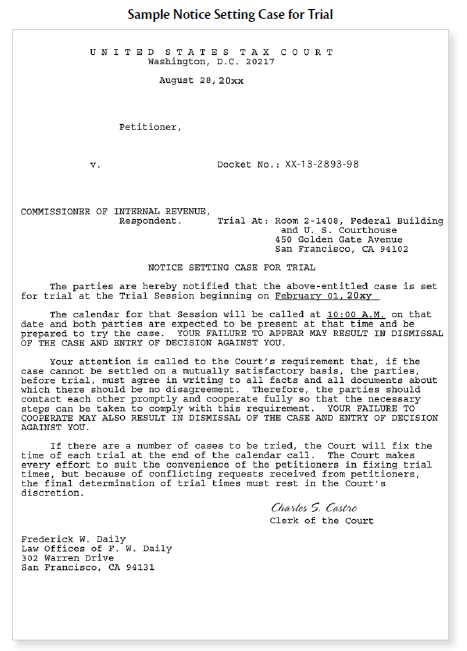

After you file your petition and receive confirmation, you probably won’t hear back from the tax court for another four to ten months. Then, you will receive a “notice setting case for trial.” It gives you the place, date, and time of your court date.

Table of Contents

Introduction

It orders you to cooperate with the IRS in certain matters before the trial. And, you are warned that if you don’t show up for the trial, your case will be dismissed.

In most cases, the trial won’t be held for at least six months or more from when you filed your tax court petition. It’s highly unlikely that a small court trial date would be more than a year from when you filed your papers.

In major cities, tax court hearings are held year-round, except summers.

In smaller places, tax court meets only once a year for a week or two.

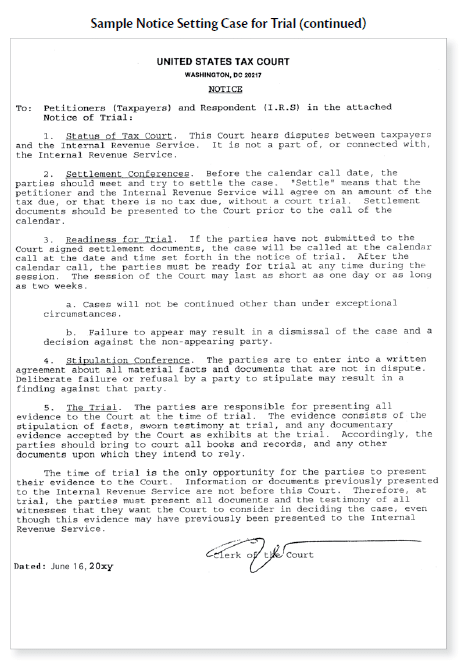

This six-to-twelve-month delay doesn’t mean that nothing is happening before your trial date. You will receive two other notices from the tax court:

Standing Pre-Trial Order

This is a notice from the judge assigned to your case. It comes three or four months prior to your trial date and orders you and the IRS to discuss settlement (see below), and states that if you don’t compromise, you must prepare written stipulations (again, see below).

The notice will advise you that obtaining a postponement of the trial date is not easy.

Finally, you are told that at least 15 days before the trial date you and the IRS must exchange lists of witnesses who may testify.

Trial Memorandum

Several months before your trial date, you’ll be sent a blank trial memorandum form and told to complete and mail it to the tax court at least 15 days before the trial.

On the form, you must state the issues to be decided by the court, the names of your witnesses, a brief summary of what they will say, and an estimate of how long the trial will last.

TIP

Don’t be concerned about mistakes when filling out this form. The judge realizes you aren’t an attorney. If you are worried about completing it—maybe forms scare you—ask a tax pro for help.

Either way, the judge doesn’t expect more than the minimum. Take a look at the filled-in sample and follow the steps outlined below.

How to Complete a Trial Memorandum

Starting at the top, notice that you are always the “Petitioner” and the Commissioner of Internal Revenue is always the “Respondent”.

Under Name of Case, write your (and your spouse’s, if applicable) name.

Under Docket Number, write the number that’s on the notice from the tax court.

Write “none” in the space for the petitioner’s attorney.

Leave blank the space for the name of the respondent’s attorney.

1. Amounts in dispute

Take this information from paragraph 3 of your petition.

2. Stipulation of facts

Below, under “Meeting With the IRS Before the Trial,” we’ll explain stipulations.

If the IRS has completed the stipulations by the time you send back this form, check “completed.” Otherwise, check “in process.”

3. Issues

Take this information from paragraph 4 of your petition.

4. Witnesses you expect to call

Give their names and addresses, along with one or two sentences explaining what they know about your case.

5. Current estimate of trial time

Generally, you will need at least an hour for your testimony and presentation of evidence and the IRS attorney’s questions. And, for every witness you will call, add on another half hour.

TIP

It’s all right to guess, but always ask for more time than you think you’ll need, to be safe.

6. Summary of facts

Be brief, but if you feel you must, you can attach a separate statement. Simply state what you did that the IRS is disputing.

This is not the time or place to refute anything or present your argument.

7. Brief synopsis of legal authorities

Unless you are confident of your tax research skills or have talked to a tax pro, leave this space blank. This space is used mostly to alert the judge to some exotic tax issue the judge has never likely encountered before.

Chances are, the judge has seen the issues in your case many times before.

8. Evidentiary problems

It’s not necessary to fill this in. But, if you think you might have a problem getting a witness to court on the date of the

trial notice, bring it up.

9. Do you wish to discuss this case with the settlement judge?

This question is not in every form. If it is on your form, say “yes.” Sign and date the form, and mail it back to the tax court.

We use cookies and similar technologies to improve site performance, security, and analytics. You can accept or manage your preferences. See our Privacy Policy and Terms of Use for Details.

Cookie Preferences

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Name

Description

Duration

Geolocation Config

This cookie is used to store the consent settings based on the visitor's location.

30 days

Cookie Preferences

This cookie is used to store the user's cookie consent preferences.

30 days

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Name

Description

Duration

cookiePreferences

Registers cookie preferences of a user

2 years

td

Registers statistical data on users' behaviour on the website. Used for internal analytics by the website operator.

session

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager

1 minute

You can find more information in our Privacy Policy and .