As an estate planning attorney, I see all the benefits a properly organized estate can offer on a daily basis. The benefits of estate planning aren’t likely as evident to others and I wanted to help share some information on what an estate plan is, the benefits it offers, and how to get started.

What is Estate Planning?

Estate planning is the creation of a definite plan for managing your wealth while you’re alive and distributing your wealth after your death. When we talk about an estate, we mean all assets of any value that you own, including real property, business interests, investments, personal property, and even your personal effects. These assets may be owned by you separately or jointly with others. Below are some examples of how married couples often hold property:

- Separate Property: Entire interest owned by one of the spouses. Property was generally acquired prior to marriage or was a gift or inheritance to one spouse alone after marriage.

- Joint Tenancy: Individual interest owned by any two or more people in which the survivor acquires the entire interest upon the death of the other joint tenants.

- Community Property: Undivided 1/2 interest owned by each spouse.

What Evils can Proper Estate Planning Prevent?

All of us face three principal obstacles—or evils—in planning our estates:

- Living Probate – the expensive court proceeding to manage your assets if you are incapacitated. This is also known as a guardianship;

- Death Probate – the expensive court proceeding to manage and distribute your assets at death; and

- Death Taxes – the taxes the government demands at your death.

All three of these evils can be completely avoided if you have a proper estate plan.

What are your Estate Planning Options?

When deciding how to handle your own estate planning, you have the following options:

- Do nothing;

- Hold title to your assets in Joint Tenancy;

- Create a Will; or

- Establish a Revocable Living Trust

This article will walk you through a discussion of each of the estate planning options and explain what happens if you do nothing, plan with joint tenancy, plan with a simple will, or set up a living trust.

What Happens if you Don’t do Estate Planning?

Believe it or not, a majority of Americans choose to do nothing. Experts report that 70% of all Americans have no written estate plan. And, of those have planned, most have created a simple will or rely on joint tenancy ownership of their assets to distribute their estate.

Unfortunately, for the majority who have no plan in place, state law will dictate how their estate is to be distributed at death. As you might imagine, the government’s plan of distribution has no particular concern for the best interests of your family. The cousin you haven’t talked to in twenty years may end up receiving the bulk of your estate.

Example: Barney Rubble refused to do any estate planning. He figured that his life-long partner would receive his assets if he passed away. Barney was in a tragic accident while working at Slate Rock and Gravel Company. Instead of his assets passing to his life-long partner, Barney’s assets passed by state law to his brother that he hadn’t talked to in more than ten years.

Also, a lot of people don’t realize that when you no plan in place, attorneys end up making much more money. This can also happen if you just have a simple will or if you hold title to all of your assets in joint tenancy.

Example: Barney Rubble and his life-long partner own a house together as Joint Tenancy With Right of Survivorship (JTWROS). Owning the house as JTWROS means that if Barney or his partner die before the other, the survive receives the house without the house going through probate.

Barney and his partner both pass away after a tragic accident while driving around Bedrock. Since both co-owners passed away, the property will need to pass through probate before the house is distributed to any beneficiaries. Probate is where attorneys charge an arm and a leg.

What is Joint Tenancy and Why do so Many People Use It?

Joint tenancy ownership is where two or more people hold title to an asset together. But unlike other forms of joint ownership, upon the death of one of the owners, the entire interest passes automatically to the surviving joint tenants. The full name for joint tenancy is Joint Tenancy With Right of Survivorship (JTWROS). Right of survivorship just means that whoever dies last owns the whole property.

Note: If you are married and a Florida resident, you should own all of your joint assets as Tenants by Entirety (TBE). This type of ownership gives spouses an extra layer of asset protection for their assets. JTWROS provides zero asset protection.

Because a joint tenant’s interest passes to the surviving joint tenants immediately at death, the deceased joint tenant’s interest is not controlled by the owner’s will. The deceased joint tenant’s interest passes by operation of law.

Example: Barney Rubble and his life-long partner own a house together as JTWROS. Barney passes away after a tragic accident at the Slate Rock and Gravel Company. Barney’s interest in the property automatically transfers to his life-long partner without the asset passing through probate.

Is Creating a Will a Good Estate Plan?

Many people plan their estates by creating a document called a Last Will and Testament. A will is simply a document that lays out how you want your assets to be distributed at death. We like to say that the will is a one-way ticket to probate court because any assets that pass through your will must go through probate.

A will also doesn’t control the distribution of all your assets. Assets owned by joint tenancy and any assets you have with a beneficiary filled out will all pass outside of your will. Wills don’t take effect until you do so they are not helpful with your lifetime planning. It’s very common that when someone dies, the will does not even need to be filed with the court since none of the deceased’s assets will pass through the will.

Upon your death, your will becomes a public document and is often filed with the probate court. It is available to anyone who wants to read it. Once your will is filed with the probate court, if you have any assets that must pass through your will, then the probate process takes over. Your estate is no longer controlled by your family. It’s in the hands of the court and the probate attorneys. Because a will is a one-way ticket to probate court, it’s a very poor estate planning document for most families since probate is very expensive and time-consuming.

Example: Barney Rubble passed away in the County of Bedrock. His only estate plan was a simple will. Because all of Barney’s assets needed to pass through his will, his spouse had to hire an attorney to put Barney’s assets through probate. The probate cost Barney’s spouse thousands of dollars and it took many months before Barney’s spouse received the assets.

Why Establishing a Revocable Living Trust is a Great Estate Planning Technique

A revocable living trust is a complete will substitute. It can control all of your assets during your life and after your death. Here’s how it works: when you create a living trust, you then transfer the title of all your major assets (stocks, bonds, real estate, etc.) from your name to the name of your trust. You then name yourself as the trustee and as the beneficiary.

That gives you, and you alone, total and complete control of all your assets. You can buy, sell, trade, and do whatever you want with the assets in your trust. Just as you do now. Even how you file your taxes does not change.

Here’s why a revocable living trust is often the preferred estate planning method over a simple will: When you die, there be no assets left in your name. With no assets left in your name, none of your assets will go through probate. No probate means your beneficiaries will save thousands of dollars and save many months of headaches.

Once you die your successor trustee will immediately gain control of your assets to distribute them according to the instructions in your trust.

Living Probate – Also Known as Guardianship

When you mention the word “probate,” most people think it’s only something that happens when you die. Unfortunately, a similar form of probate can also happen while you’re alive. It’s often referred to as Living Probate, but it’s technically called a conservatorship or guardianship proceeding.

If you become mentally disabled before you die, the probate court will appoint someone to take control of all your assets and personal affairs. These court-appointed agents must file strict annual accountings with the court. The entire procedure is expensive, time-consuming, and humiliating.

Example: Barney did not do any estate planning and become incapacitated after suffering an injury at the Slate Rock and Gravel Company. Since Barney did not have any estate planning documents his spouse had to seek a guardianship for Barney so that she could handle his health care decisions and handle his finances. This guardianship cost Barney many thousands of dollars.

Tip: Everyone over the age of 18 should have a Durable Power of Attorney and a Health Care Surrogate in place. If these documents are drafted properly they can help avoid a guardianship.

Does Joint Tenancy avoid Guardianship?

No. Each joint tenant is required to sign documents on all major transactions involving joint property. If one of the owners is mentally disabled and incapable of handling financial matters, everything will have to wait until the probate court takes control. The court basically becomes a joint owner and will continue to have a voice in managing the property until the disabled owner recovers or dies.

Does a Will Avoid Living Probate?

No. A will has no control over the events during your life.

Many people believe that just having a will is enough to protect them both during their lifetime and after they pass. Unfortunately, a will only takes effect at the time of your death. And the will is only a document that distributes your assets to your named beneficiaries when you die.

Example: Barney and his spouse only executed simple wills for their estate planning. Barney was incapacitated while driving around in Fred Flinstone’s car. Despite the fact that Barney and his spouse were married for 20 years, his spouse was unable to manage Barney’s assets or even talk to Barney’s insurance companies because Barney did not execute a durable power of attorney, nor did he execute a health care surrogate.

Result: Barney’s spouse must hire an attorney and seek a living probate—formally known as a guardianship— before she can make decisions on Barney’s behalf. Barney will receive a court-appointed attorney. Just setting up the guardianship will cost Barney and his spouse anywhere from $5,000 to $10,000. The guardianship could have been completely avoided if Barney had a well-drafted durable power of attorney and a health care surrogate.

Probate at Death – How Does Probate in Florida Work?

When you think about it, probate is not difficult to understand. When you die, your assets need to be distributed to your beneficiaries, your debts need to be paid, and any other loose ends need to be tied up. Since you are deceased, you can’t sign the deeds, write the checks, or handle your business affairs. The probate court takes over those duties.

The probate process is a long, very expensive, complicated, and bureaucratic nightmare for most families. It’s often said that only the attorneys and creditors win during a probate. Attorneys can charge roughly 3% of the probate estate as a reasonable fee under the statutes. Creditors can also wipe out an estate if there is a significant amount of debt. It is not rare to see an estate with thousands of dollars of medical bills.

Here are the five basic steps to settling an estate:

Step One: Filing the Petition and Gathering Material

A formal written petition along with a filing fee must be submitted to the court to start the probate process. One of the probate court’s first job is to approve or appoint someone to handle the affairs of the estate. This person is called the executor, administrator, or personal representative depending upon the rules of the state and whether the decedent died with or without a will. In Florida we typically refer to the person who is handling the estate’s affairs as the personal representative.

Step Two: Publishing Notice to Creditors

The second major job of the probate court is to order that the decedent’s creditors be notified so that they can present their claims to the court for payment. This requires the time-consuming task of cataloging all of the decedent’s liabilities. The creditors are either notified either by notices in the local newspaper or directly by mail. The law sets a time that the probate proceeding must be left open to allow creditors the chance to present their claims. In most states, the creditor period is several months long. The creditor period in Florida is three months.

Step Three: Inventory and Appraise Assets

During probate all the assets in the estate are usually frozen so that an accurate inventory and appraisal can be made. This means that during this period none of the assets can be distributed or sold without written permission from the court. The court will often require formal written appraisals for many items, such as real estate, antiques, collectibles, automobiles, furniture, and other valuable assets. Appraisal fees can be expensive and, like all expenses, are paid for out of the estate.

Step Four: Payment of Debts, Claims, and Taxes

Once all the debts and claims have been submitted and approved, they’re presented to the court for approval to pay them from the assets of the estate. Some states may also have death tax liability and the probate must stay open until those taxes are paid.

During the entire probate process, disgruntled heirs or those who disagree with the provisions in the will can bring a lawsuit in the probate court. These suits are called will contests. They can hold up the distribution of the estate and are often used to intimidate heirs into settling cases that have no merit.

Step Five: Final Distribution and Closing of Estate

Finally, after the court is satisfied that all legal requirements have been met, it will order all debts, claims, taxes, attorney’s fees, and the personal representative’s compensation and any other miscellaneous expenses to be paid. If there’s not enough cash in the estate to pay these substantial claims, the judge can order that assets be sold at public auctions or estate sales. These transactions are often conducted in a depressed market or under the banner of “distressed sales.”

Only after all the bills are paid, will the probate court distribute the estate to the beneficiaries named in the will, or if there is no will, to the designated heirs at law. The court then closes the file.

How Much Does Probate Cost?

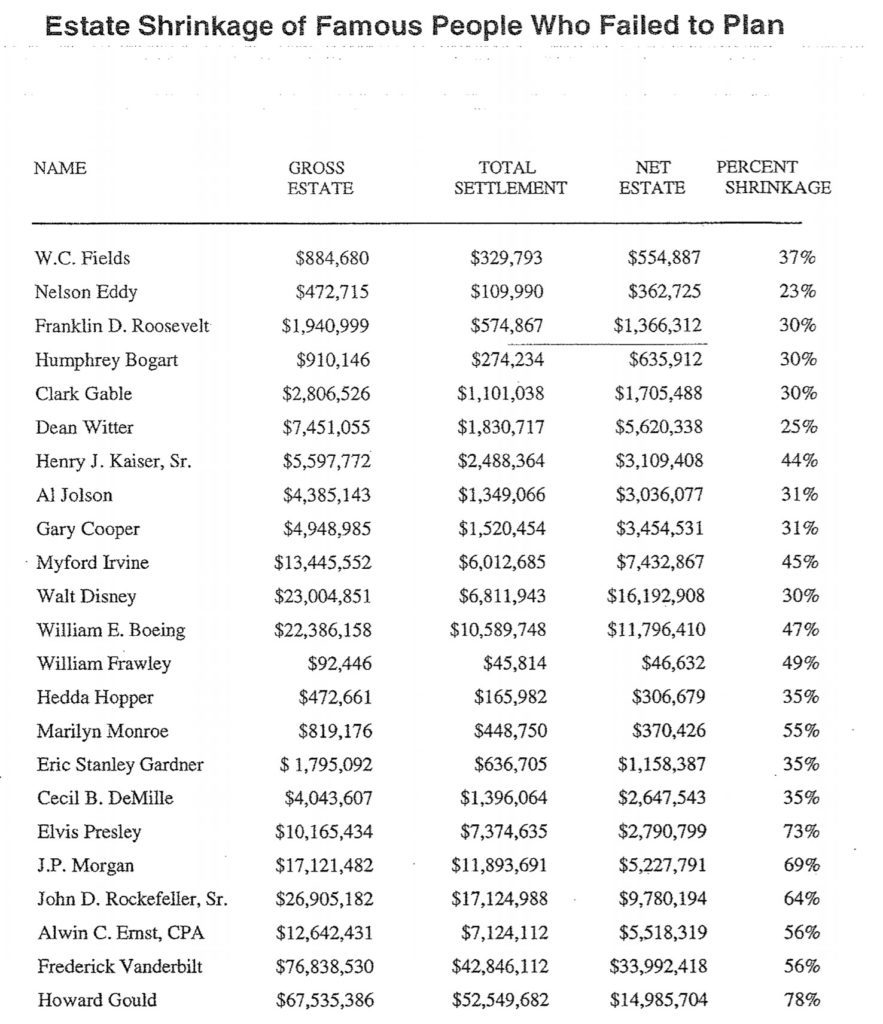

Despite what probate lawyers say, probate is very expensive. One critic of the system says that the average cost is over seven percent of the gross value of the estate. A full sixty percent of the costs go to lawyers and forty percent to personal representatives and court costs.

One legal scholar who urges a reform in the probate system remarked that “the cost of probate expands to consume the money available.” The probate system was designed so that lawyers make money and creditors are repaid for their debts. Many estate planning lawyers in Florida have made a small fortune just by drafting simple wills for clients and not do any additional planning so that assets avoid probate.

Small estates are particularly vulnerable because even reasonable fees can eat up a large percentage of an estate’s assets. There just isn’t that much to go around.

Remember, every dollar that goes to pay probate costs is a dollar that could have been distributed to your family!

Example: Barney passed away with a simple will. He had a home worth $300,000 and a bank account worth $100,000 that was solely in his name. His family had to hire an attorney to put the assets through probate. The attorney charged 3% of the estate and the personal representative also charged 3%.

Result: The attorney and personal representative will each make $12,000 from probating Barney’s assets. Including court costs, the probate will cost Barney’s family $25,000. Barney’s family could have saved $25,000 if Barney had done more estate planning than just having a simple will.

How are Probate Fees Calculated in Florida?

The way probate fees are calculated can be exceedingly unfair to your family. State laws set the probate fees that attorneys and personal representatives can charge. Many states allow attorneys to charge any fee that the court considers reasonable, without any limitations.

Other states limit the fees to a fixed percentage of the estate. Under either method, the fees can range conservatively from 6% to 10% of your family’s gross estate. Remember, probate fees are often levied at each spouse’s death. Depending on how title was held on the date of death, a married couple could pay some form of probate fees on the death of each spouse.

Not only are these fees excessive, but also the manner in which they arrive at the size of your estate bears little resemblance to its actual value. In States that use the percentage of the estate method, probate fees are calculated on your estate’s gross value without deductions for liens or encumbrances. This means that if you have property worth $200,000 but owe $150,000 to a bank or some other financial institution, your probate fees will be based on the full $200,000, not the $50,000 equity interest you actually own. As you can see, this valuation method unfairly increases the size of your estate and results in the payment of larger fees.

Caution: Florida allows attorneys and personal representatives to charge 3% each up to a million dollars.

How Long Does Probate Take in Florida?

The slow progress of your estate through probate can be very frustrating for the family. Most people assume that their estates are simple and will glide through the system. Unfortunately, this complex process can take at least seven (7) months to complete. Many estates take years.

Regardless of how simple an estate appears, it’s very difficult to close a full probate in much less than a year. That’s because of all the steps that must be completed to the satisfaction of the court.

Does Joint Tenancy Avoid Probate in Florida?

Well, the answer is yes and no. In the case of a husband and wife who own their assets in joint tenancy, there’s no probate when the first spouse dies because title passes automatically to the surviving joint tenant. However, when the surviving spouse, or when both spouses die, there will be a probate when assets are owned by joint tenancy.

The fact that joint tenancy ownership avoids probate at the first spouse’s death is a small reward for the many other disadvantages of joint tenancy ownership. It can lead to huge unexpected liability when parents and children own assets together. In community property states it creates capital gains tax problems. It can also create unintended beneficiaries. And it can cause gift and death tax problems. For these reasons, joint tenancy may not be the best way to own assets.

Tip: If you’re married and are a Florida resident, you should speak to your estate planning attorney about owning your joint assets as Tenants by Entirety (TBE). Tenants by Entirety gives a layer of asset protection to your jointly owned assets that a typical joint tenancy does not offer.

Other Issues with Probate in Florida

Perhaps the most important disadvantage of probate when you die is that your family loses control of the estate. During probate, it may not be able to sell assets without court approval even if it needs the money. Opportunities can be lost because the cumbersome probate system moves so slowly.

Your family may pay an emotional price in probate as well. Because the process takes so long, it can be a constant reminder of the loss of a loved one. Probate can also foster arguments among family members who would normally seek support from one another. It’s common to see family members taking out their frustration about the system on one another, especially if one of the family members has been named the personal representative of the estate.

Probate also gives an opportunity for family members to fight over assets. When assets pass through the will and go through the court system, it’s not uncommon for family members to bicker about the decedent’s decisions. Bickering can also lead to more attorneys getting involved, which makes the probate process more expensive and much more time-consuming.

What Happens When There’s Real Estate in Multiple States?

A probate must be instituted not only in the state where you lived but also in every state where you owned real estate. This is called an ancillary probate. Each state has probate jurisdiction of the real property located within its borders. That means that your family will have to file a new probate in each state and hire local counsel to represent the estate. Of course, this will add to the expenses that must be paid before your family receives its share. The lawyers become the real winners.

Tip: A revocable living trust is a great planning tool when you own property in multiple states. You then deed the property to the revocable living trust. If something happens to you, the property will pass to your beneficiaries without going through probate.

Does a Will Avoid Probate?

No. In fact, a will guarantees probate. The word probate is actually Latin, and it means “to prove the will.” All property that is controlled by your will must go through the probate court. Once your estate enters the probate process, it’s trapped in the system until the judge releases it.

Does a Living Trust Avoid Probate?

Yes. All assets transferred to a living trust completely avoid the probate process, both during your life and at your death. Living trusts are not new. They’ve been successfully used in one form or another since the Middle Ages. Both then and now, the living trust has required that the owner of assets transfer tile from his or her name to the name of the trust. This means really changing the title to your property. For real property, it means you will sign a new deed transferring the property from your name to your living trust. For other assets, you sign special transfer documents changing ownership to the name of your trust. Once the process is complete, all of your assets will be owned by your trust.

Almost nothing will be owned by you personally. Your living trust has title to the assets. But don’t worry, you have complete control of the trust while you’re alive. You can amend the trust or even revoke it whenever you like. But when you die, there are no assets in your name so there’s no need to go through probate. The trust already has your written instructions directing your handpicked agent, the successor trustee, about how you want your estate distributed.

With a living trust, there’s no need for “help” from the probate court or probate lawyers. Your trust will eliminates these unnecessary costs. Moreover, your estate can be distributed instantly at your death. There are no judges to consult or bureaucrats to please. Your trustee merely follows your instructions in distributing your estate according to your wishes.

What are Death Taxes – Also Known as the Estate Tax?

In addition to the expense and delay of probate, your family may also be liable for death taxes. There are two types of death taxes: the federal estate tax and the state inheritance tax. Many states have abolished the inheritance tax but the federal estate tax is still around and it’s one of the largest taxes a family will ever have to pay. It’s a tax on your right to transfer property to others at your death. Currently, the federal estate tax rate is a flat 40%. This means that every dollar over the estate exemption is immediately taxed at 40%.

Example: Barney’s estate is $200,000 over the estate tax exemption. That means that the $200,000 will be taxed at the 40% federal estate tax rate, resulting in an estate tax of $80,000. Ouch!

Do all Estates Pay Federal Estate Taxes?

No. The federal government has given every person in the United States an exemption of $11.4 million (2019) per person. That means if your estate, at the time of your death, is less than $11.4 million, there will be no federal estate taxes due. In deciding whether your estate is greater than or less than $11.4 million, the government will include everything you own, all the gifts you’ve made during your life, and the face value of your life insurance policies.

You may be asking yourself if the estate tax is $11.4 million why do I need to worry about the estate tax? Well, there are two reasons. The first reason is that the current estate tax will sunset after 2025. That means that on 2025 the estate tax will automatically revert back to $5 million. If your estate is close to or above $5 million, you may want to take advantage of gifting to remove assets from your estate. Any gifts made with the current exemption of $11.4 million will be grandfathered in if the estate tax goes lower.

The second reason why you should worry about the estate tax is that the estate tax largely depends on which president is in office and the current political climate. It wasn’t too long ago that the estate tax was $675,000 (2001). The estate tax can always change. If you have an estate in the millions, you may want to consider some proactive estate tax planning.

Should I Worry about Estate Planning if I Have a Small Estate?

Yes. While the estate tax exemption is currently very high and only affects a very small percentage of Americans, your estate may be subject to a guardianship or probate if you’re incapacitated or if you die. Remember, the estate tax has nothing to do with a guardianship or a probate. Estate taxes are paid to the federal government for the right to transfer property at your death. Guardianship and probate fees and costs are paid to the probate court, attorneys, and the personal representatives of your estate for supervising the administration of your estate and distributing assets to your beneficiaries.

How Can I Create a Living Trust?

The first step in determining whether a living trust is a good option for your estate planning needs is to meet with a competent estate planning attorney. Most estate planning attorneys offer a free initial consultation. The estate planning attorney should discuss the following issues with you during your initial meeting:

- How your assets are to be distributed after your death;

- The names of the people you want to manage your assets if you become mentally disabled, and if you die;

- How to protect your assets;

- How to avoid probate for all of your assets; and

- Long term care solutions such as Medicaid planning or purchasing a long term care policy

Benefits of a Revocable Living Trust

If you become disabled or are unable to manage your estate, your living trust avoids the need for a court-mandated guardianship. The successor trustee you’ve named will step in and manage your affairs without government interference and expense. Avoiding guardianship will save you anywhere between $5,000 to $10,000 dollars.

Example: Barney sets up a revocable living trust and placed all of his assets in the trust. Barney became incapacitated after an accident while working at Slate Rock and Gravel Company. His successor trustee, Fred Flinstone, immediately stepped into Barney’s shoes to manage Barney’s assets. This saved Barney many thousands of dollars because he did not need a guardianship.

Caution: Creating your own revocable living trust is very dangerous. When things are set up properly, attorneys make much more money. Sites like LegalZoom only make attorneys more money because most documents are poorly drafted and estates are not properly planned.

A Revocable Living Trust Avoids Probate at Death

With a living trust, your assets will go directly to your beneficiaries after your death. Everything that is titled in the name of your trust is no longer titled in your name, so there will be no probate, attorney’s fees, or court costs. There will be no delay in distributing your assets, and all of your distributions will be private.

A Revocable Living Trust Can Reduce or Eliminate Federal Estate Taxes

With a living trust, a married couple can pass over $22 million absolutely estate tax-free to their heirs. A single person can pass over $11 million estate tax-free. Additionally, your beneficiaries receive a full step-up in basis on the assets of the trust, meaning that they will not owe any capital gains taxes on your assets if they sell the assets right after you pass.

A Revocable Living Trust Allows You to Restrict How Your Estate is Managed and Spent Even After Your Death

It can provide for the care, support, and education of your children by turning over assets to them at an age chosen by you. Even insurance proceeds can be paid to the trust so your successor trustee can manage them for the benefit of your family.

A Revocable Living Trust Can Protect Assets for your Beneficiaries

A well-drafted revocable living trust can protect your assets from your beneficiaries’ creditors. These creditors can be from ex-spouses, unpaid credit card bills, or lawsuits from a car accident.

A Revocable Living Trust Gives You Peace of Mind

When your living trust is completed, you and your family will relax knowing that your estate will be managed and distributed by someone you have selected and trust.

Frequently Asked Questions About Revocable Living Trusts

Can I act as my own trustee?

Yes. If you are competent to handle your financial affairs now, there’s no legal reason you cannot be the trustee of your own revocable living trust. In fact, most living trusts have the people who created them acting as their own trustees. If you’re married, you and your spouse can act as co-trustees.

What can I do with my assets once they’re in my revocable living trust?

If you’re the trustee, you can do anything you want with the trust assets. When you set up your living trust, you are transferring the title of all your assets from you as an individual to yourself as trustee of your trust. You then must manage the property for the benefit of yourself as the beneficiary.

What this means is that you will have absolute and complete control over all the assets of your trust. If you want, you can spend, save, invest, or even give the assets away at your discretion. There are no restrictions on what you can do with the assets in your living trust. Moreover, if you don’t like the terms of the trust, you can amend it or revoke it any time without penalty.

Will my taxes change with a revocable living trust?

No. Your taxes will not change with a revocable living trust. And your taxes will not be more difficult. You will file your income tax returns in exactly the same way you filed them before the trust existed. There are no new returns to file and no new tax liabilities are created.

Will my revocable living trust avoid income taxes?

No. The purpose of creating your revocable living trust is to avoid a guardianship during your life, probate at your death, reduce or eliminate federal estate taxes, and protect your assets for your beneficiaries. It’s not a vehicle for reducing income taxes.

If I transfer real estate into my revocable living trust, will I lose my homestead exemption?

No. Transfers into your living trust do not affect your homestead exemption if you have the right homestead language in your trust.

Will transfers of real estate into my revocable living trust cause my property taxes to go up?

No. Transfers into your living trust have no effect on your property taxes.

If I’m only a part-owner of property, can I transfer my share into my revocable living trust?

Yes. Your share can go into the trust without changing the interests owned by others.

Can I name trustees and beneficiaries who live out of state?

Yes. There is no limitation on where your trustees or beneficiaries must reside.

Will I have to consult an attorney every time I buy new assets?

No. Once your current assets are transferred to your living trust, you take title to all your new assets in the name of the trust and they will automatically be owned by your trust.

Does my revocable living trust need to be registered or recorded anywhere?

No. Your living trust is a private document that is not recorded. However, if you own any interest in real estate, the new deeds showing trust ownership will be recorded.

Can I sell assets owned by my revocable living trust without complications?

Yes. You sell assets in the same way you currently do. You will, however, add the word “Trustee” after your signature.

Can I change the terms of my revocable living trust?

Yes. While you’re alive and competent, you can alter your living trust or even revoke it without penalty at any time.

Can I transfer real estate into my revocable living trust?

Yes. In fact, most of your real estate should be transferred into your living trust. Otherwise, upon your death, there will be a probate at your death in every state where you own real property. When it’s owned by your living trust, there is no probate anywhere.

Is my revocable living trust just a tax loophole that the government will close down?

No. Your living trust has been authorized by the law for centuries. The government has no interest in making you go through a guardianship or a probate at death. Those proceedings only clog up the court system. The only portion of your trust that may change is the amount of the federal estate tax deduction. A properly drafted living trust will take maximum advantage of whatever that deduction may be.

Can I transfer my separate property as well as my community property into my revocable living trust?

Yes. All of your assets, both separate and community, are transferred into your revocable living trust but they are not commingled. Separate property assets retain their separate property character while in your trust. If your marriage breaks up, all assets come out of your living trust in the same way they went in: Community property is divided between the spouses and separate property is returned to the party who originally owned it.

Can any attorney create a revocable living trust?

No. The drafting of your revocable living trust should only be done by an attorney trained in the area of tax and trust law. It’s important that you seek out a law firm that focuses its practice on estate planning and the creation of revocable living trusts. Your trust will be the document that manages and disposes of all of your hard-earned wealth. It’s important that you choose a law firm that is both qualified and experienced.

Will my revocable living trust be valid in another state if I move?

Yes. Your revocable living trust is valid in all 50 states, regardless of the state where it was originally created.

Is a revocable living trust only for the rich?

No. A living trust can help anyone who wants to protect his or her family from unnecessary probate fees, attorney’s fees, court costs, and federal estate taxes. In fact, if your total estate is greater than $75,000, a revocable living trust offers substantial protection to your family and will save your family thousands of dollars in probate fees.

Is a revocable living trust a good idea for a single person?

Yes. If you’re widowed, divorced, or unmarried, a revocable living trust offers protection for your estate. It will completely avoid a probate at your death, guardianship during your lifetime, and it can help save your beneficiaries taxes.